Today's highly competitive media environment has put a dent in revenues, particularly for traditional news outlets. In the struggle to maintain profits, cutting costs was an easy first step - although it created a feedback loop, since cutting costs meant reducing the value of the product, which led to lower demand and further revenue losses. Many news media also started looking for new sources for revenues - entering new markets (going online), repurposing content for later sales, finding ways to add value to the basic product, among others. The trouble's been that few of these have turned out to be significant contributors to total revenues.

A local TV station in Orlando has come up with a new approach that could provide a new model for successfully monetizing news. Taking advantage of national interest in a local trial (the Casey Anthony murder case), they used their own coverage and their local access to create an online site to follow the case, assembling daily news reports, videos, photos, case calendar and legal documents (more than 20,000 pages of content). Access is through a paid iPhone app, which also serves to push updates to interested mobile users. The effort's been successful, topping the paid news apps category for weeks. While not divulging actual sales numbers, WESH-TV's digital media manager Gabe Travers, thought the app was a natural extension of the broadcaster's extensive coverage.

The way they've approached this app has also contributed to the app's success. First, there was a focus on a big story with broad interest, rather than items of general, but passing, interest. In many ways, a narrow focus makes it easier to establish value, if only for the portion of audience that is interested. Second, they loaded up the content side, and included the kinds of background and supporting material that would never make a regular newscast and are also not easily available elsewhere. Loading up on content helps in several ways - it expands the potential market (for example, Travers noted that the legal documents were surprisingly popular, perhaps tapping into the legal market), and bundles limited interest in specific pages to levels of aggregate value that are more likely to exceed the cost of access. Finally, they kept the price low, making it easier for people to try it out, to find that there is sufficient value, and to recommend it to others.

Now not every media outlet has a high-profile story with national or international interest that they might be able to exploit in this fashion. But WESH-TV's success should encourage other media outlets to think about what stories or content might find an audience willing to pay a little for access to more content and information than is generally available.

Source: "Local TV iPnone app tops the iTunes charts," Lost Remote

Thursday, June 30, 2011

Wednesday, June 29, 2011

Collaborative Journalism Projects

I'm spending the next couple of days at a symposium here at the University of Tennessee, Knoxville, on the various collaborative Innocence/Wrongful Conviction Projects that combine the efforts of students, faculty, and staff at Law Schools and Journalism Schools. There are several around the country, and we're working on starting a similar collaborative effort here (the Law School here has one, and approached the School of Journalism about working together to expand their efforts).

Other than bragging, the purpose of this post is to talk about such projects as examples of what's called collaborative journalism - where reporters collaborate with other reporters or outside experts, who may be able to bring particular expertise and/or resources to the investigation of stories, and/or citizen journalism, where investigations and stories are produced by "non-professionals". There's a number of other good examples of collaborative journalism, although traditionally the collaboration was limited to a small group of reporters from different beats working together on a story, or a reporter relying on some outside expert to help understand what information an investigation revealed. Collaboration was primarily limited and short-term, and citizen journalism was largely discounted as being non-professional, and thus of no value.

Today, the rise of the Internet, with its ability to facilitate communication, and services that make true collaboration easier (for example, Wikis), is making it easier to develop larger and more permanent collaborative efforts. At the same time, academia has been increasingly emphasizing collaborative efforts, and recognizing that different fields can bring different expertise and skill sets to investigations. Particularly when the subject is inherently interdisciplinary, as is the case with the idea of looking into potentially wrongful convictions. The Web also has enabled citizen journalism, not only by facilitating access to sources and materials, but by providing a venue to report and share results.

Still, there's not been a high degree of collaborative journalism being done by "professional" journalists in traditional media - the few joint Law School/ Journalism School projects rely on students, overseen by faculty (some of whom are former professionals). Yet these "citizen journalists" have often out-reported the local professionals, and had a larger impact on communities and individual's lives. One would think that "professional journalism" - reporters and news organizations - would be better served to embrace collaborative and citizen journalism, if only that it's taking advantage of free labor, and to save themselves from the potential embarrassment of being scooped. The kind of projects we're hearing about today at this symposium would seem to be a very good place to start. These projects have an enviable track record and reputation, on issues of clear relevance and importance to the communities news organizations serve. As news organizations continue shrinking their own investigative units, support of, and collaboration with, these projects would be a good investment.

Other than bragging, the purpose of this post is to talk about such projects as examples of what's called collaborative journalism - where reporters collaborate with other reporters or outside experts, who may be able to bring particular expertise and/or resources to the investigation of stories, and/or citizen journalism, where investigations and stories are produced by "non-professionals". There's a number of other good examples of collaborative journalism, although traditionally the collaboration was limited to a small group of reporters from different beats working together on a story, or a reporter relying on some outside expert to help understand what information an investigation revealed. Collaboration was primarily limited and short-term, and citizen journalism was largely discounted as being non-professional, and thus of no value.

Today, the rise of the Internet, with its ability to facilitate communication, and services that make true collaboration easier (for example, Wikis), is making it easier to develop larger and more permanent collaborative efforts. At the same time, academia has been increasingly emphasizing collaborative efforts, and recognizing that different fields can bring different expertise and skill sets to investigations. Particularly when the subject is inherently interdisciplinary, as is the case with the idea of looking into potentially wrongful convictions. The Web also has enabled citizen journalism, not only by facilitating access to sources and materials, but by providing a venue to report and share results.

Still, there's not been a high degree of collaborative journalism being done by "professional" journalists in traditional media - the few joint Law School/ Journalism School projects rely on students, overseen by faculty (some of whom are former professionals). Yet these "citizen journalists" have often out-reported the local professionals, and had a larger impact on communities and individual's lives. One would think that "professional journalism" - reporters and news organizations - would be better served to embrace collaborative and citizen journalism, if only that it's taking advantage of free labor, and to save themselves from the potential embarrassment of being scooped. The kind of projects we're hearing about today at this symposium would seem to be a very good place to start. These projects have an enviable track record and reputation, on issues of clear relevance and importance to the communities news organizations serve. As news organizations continue shrinking their own investigative units, support of, and collaboration with, these projects would be a good investment.

Tuesday, June 28, 2011

Can online journalism become more reliable? (Updated)

Americans' confidence in news media has been declining for decades. The most recent report by the Pew Research Center for People and the Press (2009) suggest that less than a third of Americans think media regularly gets their facts straight, and less than one in five feels news media deals fairly with all sides when covering politics or controversies. The decline has been going on far longer than the twenty years reported by the Pew study, and has shown fairly consistent declines. And the biggest source of declining trust and reputation has to do with the perceived accuracy of news reports.

Another report by Harvard's Nieman Foundation for Journalism showed that more than half of local news and feature stories contained at least one error. More troubling, when errors were pointed out, newspapers published corrections in less than 3% of cases. The Nieman piece goes on to argue for the need to develop and follow a strong corrections policy, particularly in a digital environment. Surveys of US newspapers indicate that half of all news stories online are not copyedited - more alarmingly, one in four news outlets report that they never edit, fact-check, or proofread the online news stories they post. Only one in three editors reported copyediting or otherwise checking posts to blogs affiliated with the news site.

Another report by Harvard's Nieman Foundation for Journalism showed that more than half of local news and feature stories contained at least one error. More troubling, when errors were pointed out, newspapers published corrections in less than 3% of cases. The Nieman piece goes on to argue for the need to develop and follow a strong corrections policy, particularly in a digital environment. Surveys of US newspapers indicate that half of all news stories online are not copyedited - more alarmingly, one in four news outlets report that they never edit, fact-check, or proofread the online news stories they post. Only one in three editors reported copyediting or otherwise checking posts to blogs affiliated with the news site.

The rush to get the story out first, the ability to quickly post stories, and the general lack of oversight and pre-publication review suggest that online journalism may be error-prone. The rapidity in which stories are picked up, shared, and integrated in other news reports means that the consequences of errors propagating throughout the Web are magnified. On the other hand, it's been argued that the Web provides the opportunity for readers to point out any errors, and allows for rapid corrections to be made. How corrections are made may itself be an issue. Do revised stories just appear without notice of any change or correction (the hot phrase for that seems to be "airbrushing" stories), or are the corrections or edits specifically acknowledged, with or without maintaining the various versions of the story?

The Nieman report made some initial suggestions, indicating that making formal acknowledgments of errors and quickly making corrections not only helped improve readers' perceptions of reliability, but also had the effect of reducing the frequency of future errors. A piece in PBS' Mediashift Idea Lab by Scott Rosenberg offers more concrete suggestions:

I think Rosenberg comes to a good conclusion:

When you've lost your credibility, you've lost any value as a news organization - what's left is little more than entertainment and gossip.

Sources:

"How Newsrooms Can Win Back Their Reputations" PBS Mediashift Idea Lab

"Press Accuracy Rating Hits Two Decade Low", Pew Research Center report

"Confessing Errors in a Digital Age," Nieman Report

Edit 1: Fixed some typos.

Update (29June2011) - One day - and a new poll result from Gallup suggests that confidence in news organizations has improved - slightly (up 1-2%). And provides a new graphic.

Source: "Americans regain some confidence in Newspapers, TV News" Gallup Reports

The rush to get the story out first, the ability to quickly post stories, and the general lack of oversight and pre-publication review suggest that online journalism may be error-prone. The rapidity in which stories are picked up, shared, and integrated in other news reports means that the consequences of errors propagating throughout the Web are magnified. On the other hand, it's been argued that the Web provides the opportunity for readers to point out any errors, and allows for rapid corrections to be made. How corrections are made may itself be an issue. Do revised stories just appear without notice of any change or correction (the hot phrase for that seems to be "airbrushing" stories), or are the corrections or edits specifically acknowledged, with or without maintaining the various versions of the story?

The Nieman report made some initial suggestions, indicating that making formal acknowledgments of errors and quickly making corrections not only helped improve readers' perceptions of reliability, but also had the effect of reducing the frequency of future errors. A piece in PBS' Mediashift Idea Lab by Scott Rosenberg offers more concrete suggestions:

- Link generously - particularly to source materials

- Show your work - indicate what corrections or changes are made (or better yet, make all versions available)

- Make it easy for readers to report possible errors - harness their expertise (it's free)

Many journalists view readers as adversaries... the specific reader with a complaint is "someone with an agenda" whom they have a duty to ignore.

On the other hand, there are also some structural factors at play - once a story is out, reporters normally move on to something new, and there is little incentive in news organizations to keep returning to "old news." That approach is part of the old media emphasis of reporting to deadlines, of working to fixed editions rather than a continuing news flow. In addition, making corrections doesn't bring in revenue directly, although you could make a strong case that making corrections and improving your reputation makes a news outlet more valuable in the long run. A focus on short term revenue generation also contributes to policies against linking outside one's own site, and the failure to incorporate online features conducive to eliciting comments and corrections and versioning into content management systems.

I think Rosenberg comes to a good conclusion:

Ask journalists what sets them apart from everyone else sharing information online and we'll say: We care about accuracy. We correct our mistakes. In a changing media economy that's challenging the survival of our profession, we need to follow through on those avowals. ... But journalists will never regain public trust unless we overcome (these obstacles to correcting errors).But read all three of these reports - they ought to serve as a wake-up call for journalists and news organization.. The next Pew reputational study should be out this fall, and we'll see whether journalism continues to throw away its credibility and reputation. Given their recent performance, I expect the decline to continue. And that's very problematic to journalism's long term survival.

When you've lost your credibility, you've lost any value as a news organization - what's left is little more than entertainment and gossip.

Sources:

"How Newsrooms Can Win Back Their Reputations" PBS Mediashift Idea Lab

"Press Accuracy Rating Hits Two Decade Low", Pew Research Center report

"Confessing Errors in a Digital Age," Nieman Report

Edit 1: Fixed some typos.

Update (29June2011) - One day - and a new poll result from Gallup suggests that confidence in news organizations has improved - slightly (up 1-2%). And provides a new graphic.

Source: "Americans regain some confidence in Newspapers, TV News" Gallup Reports

E-Reader ownership doubled since Christmas

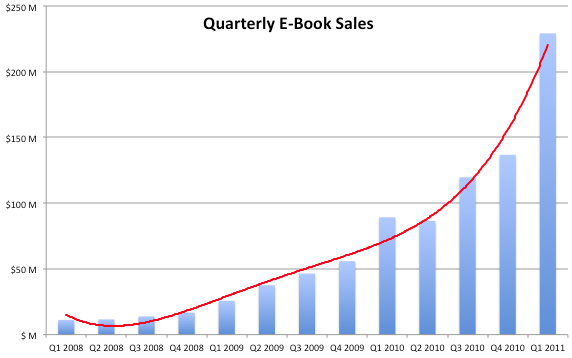

There are very few innovations where the point that critical mass was achieved can be pinpointed as clearly as it can for eBooks. Critical mass refers to the point where there are sufficient devices to encourage production of content, and their is sufficient content available to encourage acquiring the eReader devices to access the content. For eBooks, last fall saw a significant expansion in the range and variety of eReaders available, along with the reduction in costs and prices to open up demand. Sales of eReaders boomed during the Christmas season, and has continued to grow. One report had global eReader sales in the last quarter of 2010 topping 5 million, almost double that of the previous quarter. A new report from the Pew Internet & American Life Project found ownership of eReaders in the U.S. grew from 6% in November 2010, to 12% in May 2011. Between the growth in eReader availability and Amazon's leadership in offering free eReader apps for a range of computers, smartphones, and tablets, critical mass in display devices was clearly reached at some point during last Fall's Christmas season.

|

Critical mass for content was also likely reached around the last quarter of 2010, with Amazon doubling the number of eBook titles offered (with over 800,000 titles available in December, 2010, and the entry of other large eBook stores (Apple's iBook (selling 100 million books in its first year), and Barnes & Noble). The final indicator of critical mass is the explosion in eBook sales. As of last February, eBook sales in the US had tripled from the previous year, becoming the number one format among those recognized by the Association of American Publishers. The value of eBook sales in the US was being forecast to grow from around $300 million in 2009 to $2.7 billion in 2013. eBook sales are on a pace to surpass $1 billion this year.

Updated: To fix formatting issue with second graphic

Sources: "e-Reader ownership doubles in six months." Pew Internet & American Life report.

Also check out the eBooks tag in this blog's Labels cloud.

PBS Lauches Digital Media Education Site

PBS, and a number of affiliated noncommercial stations are partnering to offer a new online educational service and platform. The service, PBS Learning Media (http://www.pbslearningmedia.org/) will be made available to teachers, their students, and their families without charge. The service provides access to more than 14,000 items of educational value, including materials from PBS, the Library of Congress, the National Archives, etc.

PBS plans on introducing portals customized to local educational standards and needs, starting this fall.

This is a good example of what can be done by repackaging and repurposing content, developing new uses and markets. Also, the organization, search capabilities, and integration of supporting materials shows how value can be added to existing content, making it more discoverable and usable.

Source: "PBS Launches New Digital Media Education Platform," Multichannel News

PBS Learning Media portal: http://www.pbslearningmedia.org

PBS plans on introducing portals customized to local educational standards and needs, starting this fall.

This is a good example of what can be done by repackaging and repurposing content, developing new uses and markets. Also, the organization, search capabilities, and integration of supporting materials shows how value can be added to existing content, making it more discoverable and usable.

Source: "PBS Launches New Digital Media Education Platform," Multichannel News

PBS Learning Media portal: http://www.pbslearningmedia.org

5 Innovations changing Cable TV

Earlier this month, the cable industry held its big annual trade show (The Cable Show) in Chicago. These shows are good places to look at the new ideas and technology that drive innovation. Multichannel News' Todd Spangler identified five areas of innovation that are likely to impact the cable industry.

Source: "5 Technology Innovations Changing Cable TV" Multichannel News

- Web-User Interfaces - from developing cloud-based programming guides (providing access from any device, anywhere; the capability to personalize features, including integration with social media and other Web services like Twitter), to apps allowing users to control set-top boxes and DVRs, enhanced search capabilities, to IPTV services delivering video programming to a variety of devices, look for even more choices for people to personalize and control their viewing experiences.

- Multiscreen Video - The goal is "TV Everywhere," the idea that program can be delivered to any screen, anywhere, at any time. A variety of technologies are addressing the two key underlying issues: taking content designed for one screen and optimizing it for other screens and networks; and developing systems to ensure that content is delivered only to licensed users (the issue of authentication).

- Broadband Speed - IPTV, and all of the above services need bandwidth. Their growth, and the growth of IPTV will drive demand for higher bandwidth (Cisco forecasts average worldwide broadband speeds to grow from 7 Mps in 2010 to 28 Mps by 2015). The Cable Show saw several innovations that could cable get higher broadband speeds from its installed network.

- Home Gateways - the transition from the current mix of analog and digital signals on most cable systems to fully digital will help cable expand services - although at the cost of the signals being incompatible with existing TV sets. The current solution is to provide set-top boxes for each TV, but home gateways offer a bit of an alternative. Combining multiple tuners with high storage capacity, a home gateway becomes the primary cable-to-broadcast conversion point, feeding channel and viewing choices direct to each set through existing inputs.

- Advanced Ads - talking advantage of the interactivity and the addressability of digital cable, there's long been a promise of being able to incorporate direct user responses to ads (click on an ad to receive more info, etc.) and to more narrowly target ads (having VOD operators to insert the ads most appropriate to the program and household in the delivered content, or having your box determining which of a set of ads is most appropriate for you)

Source: "5 Technology Innovations Changing Cable TV" Multichannel News

Thursday, June 23, 2011

Local Broadcasters Try for Relevance (Fun With Numbers)

Some recent headlines in trade magazines proudly proclaimed Local Broadcast TV's massive contribution to the U.S. economy - claiming responsibility for generating $1.7 trillion annually (7% of GDP) and 2.52 million jobs. The NAB-funded study is being used to help broadcasting in policy discussions with the FCC over having to give back unused or underused radio spectrum. As NAB head Gordon Smith said, "Decision-makers now debating spectrum policies need to be cognizant of the millions of people and thousands of businesses reliant on the unparalleled impact of local TV and radio for economic survival."

So where did those totals come from?

Another problem with using general multipliers is that actual impacts are likely to vary geographically, and across different types of activities. The study may partially address this, in that the full report also breaks down impacts by state. But there's also a problem with that, as broadcast signals don't coincide with state boundaries and so any impacts can't be isolated to specific states. All this raises questions about the validity and accuracy of these estimates.

But the biggest problem is a general one with this kind of analysis. In treating these numbers as distinctive, it assumes that none of those economic activities would take place in the absence of broadcasting. That is, the 300,000 employed by broadcasting wouldn't be working or spending any money to support themselves and their families, or that the $42 billion in advertising wouldn't simply shift to other media - or if it did, then it wouldn't have any "stimulus effect" elsewhere. In claiming that broadcasting is responsible or that it generates this amount, the report is implying that in the absence of local broadcasting, all of the direct or indirect economic activity associated with broadcasting would go away. It's not a very reasonable presumption, if you think about it,

(And thinking about the "stimulus" from advertising - shouldn't that be credited to the advertisers? All broadcasters do is distribute the message. The arguments the study uses to claim a stimulus effect are almost all a result of the information content of advertising, rather than any unique aspect of local broadcasting as a distribution system. So shouldn't that almost 90% of the claimed impact generated by advertising be credited to the advertisers rather than broadcasters?).

Now, this kind of "multiplier" argument is fairly widely used, particularly by politicians and others hoping to inflate the significance of certain economic or political activities. But as long as the assumed comparison is to a total lack of economic activity, it grossly overstates the real impact that can be traceable to any particular economic activity - the difference between the impact of that activity and the impact of its alternatives. This kind of analysis is (intentionally) highly misleading. If you think about it, this argument is really saying that

To make the case that broadcasting is responsible for multiplier or "additional" activity, you really need to make a case as to how much would occur economic activity local broadcasters contribute, directly and indirectly, compared to other options - such as how much might result if the all broadcast content was to be distributed via IPTV and broadband systems, rather than local over-the-air broadcast stations. You could then realistically claim that local broadcasting is responsible for the net difference, positive or negative.

It's a nice try, though. It may work with policymakers who use the approach themselves (and also tend to be fairly ignorant of economics).

Updated: Fixed some typos, and extended discussion of "stimulus" claims.

Source: "Local broadcasting generates $1.17 trillion to annual GDP, study shows", Broadcast Engineering

Study report: "An Analysis of the Importance of Commercial Local Radio and Television Broadcasting to the United States Economy."

So where did those totals come from?

- $60 billion and 300K jobs come from broadcasting, or from industries that support the broadcast industry (that's 3.5% of the claimed total that comes more or less directly from broadcasting)

- $135 billion and 833K jobs come from multiplier effects (the ripple effect that comes from broadcasting's employee spending).

- $986 billion and 1.38 million jobs come from "the additional economic activity generated ... as a forum for advertising goods and services." What's that? - I'm guessing they are measuring a portion of all the economic activity that advertisers engage in. The study gives a number of reasons for counting stimulative activity, but no information on how those numbers are derived. In essence, it seems likely that they've come up with another multiplier effect. (Not indicating how these numbers were derived is frowned upon in academic research)

Another problem with using general multipliers is that actual impacts are likely to vary geographically, and across different types of activities. The study may partially address this, in that the full report also breaks down impacts by state. But there's also a problem with that, as broadcast signals don't coincide with state boundaries and so any impacts can't be isolated to specific states. All this raises questions about the validity and accuracy of these estimates.

But the biggest problem is a general one with this kind of analysis. In treating these numbers as distinctive, it assumes that none of those economic activities would take place in the absence of broadcasting. That is, the 300,000 employed by broadcasting wouldn't be working or spending any money to support themselves and their families, or that the $42 billion in advertising wouldn't simply shift to other media - or if it did, then it wouldn't have any "stimulus effect" elsewhere. In claiming that broadcasting is responsible or that it generates this amount, the report is implying that in the absence of local broadcasting, all of the direct or indirect economic activity associated with broadcasting would go away. It's not a very reasonable presumption, if you think about it,

(And thinking about the "stimulus" from advertising - shouldn't that be credited to the advertisers? All broadcasters do is distribute the message. The arguments the study uses to claim a stimulus effect are almost all a result of the information content of advertising, rather than any unique aspect of local broadcasting as a distribution system. So shouldn't that almost 90% of the claimed impact generated by advertising be credited to the advertisers rather than broadcasters?).

Now, this kind of "multiplier" argument is fairly widely used, particularly by politicians and others hoping to inflate the significance of certain economic or political activities. But as long as the assumed comparison is to a total lack of economic activity, it grossly overstates the real impact that can be traceable to any particular economic activity - the difference between the impact of that activity and the impact of its alternatives. This kind of analysis is (intentionally) highly misleading. If you think about it, this argument is really saying that

To make the case that broadcasting is responsible for multiplier or "additional" activity, you really need to make a case as to how much would occur economic activity local broadcasters contribute, directly and indirectly, compared to other options - such as how much might result if the all broadcast content was to be distributed via IPTV and broadband systems, rather than local over-the-air broadcast stations. You could then realistically claim that local broadcasting is responsible for the net difference, positive or negative.

It's a nice try, though. It may work with policymakers who use the approach themselves (and also tend to be fairly ignorant of economics).

Updated: Fixed some typos, and extended discussion of "stimulus" claims.

Source: "Local broadcasting generates $1.17 trillion to annual GDP, study shows", Broadcast Engineering

Study report: "An Analysis of the Importance of Commercial Local Radio and Television Broadcasting to the United States Economy."

Changing Audience Habits: Teens Today

A recently released Nielsen study of the media habits of teens (ages 12-17) indicated that:

None of this is really new - it's a continuation of trends over the last ten years or so. But it's another call for traditional media to rethink it's conventional audience model - where the media users are passive, anonymous, receptors of whatever content the media outlet chooses to deliver. A new audience choice model is emerging.

Source: "Teen Media Behavior; Texting, Talking, Socializing, TV Watching, Mobiling." Research Brief from the Center for Media Research

- Text more frequently than any other age group (twice as much as nearest demo), and talk less on the phone. 77% of teens have their own mobile phones, and another 11% regularly borrow one.

- Almost 80% use social media or blogs

- Are the heaviest viewers of mobile video (over 7 hours/month), but watch traditional TV less than other age groups

- Even so, their TV viewing is up slightly, and Internet use down slightly - although their Internet use is more highly targeted.

- Only 1 in 4 read a newspaper

None of this is really new - it's a continuation of trends over the last ten years or so. But it's another call for traditional media to rethink it's conventional audience model - where the media users are passive, anonymous, receptors of whatever content the media outlet chooses to deliver. A new audience choice model is emerging.

Source: "Teen Media Behavior; Texting, Talking, Socializing, TV Watching, Mobiling." Research Brief from the Center for Media Research

Tuesday, June 21, 2011

WHYY Tries Online News

Old-line Philadelphia public broadcaster WHYY has invested more than a million dollars towards last November's launch of NewsWorks.org, a website offering a mix of hyperlocal news, community partnerships, and civic and cultural reporting, combined with numerous layers of calls for user engagement. To date, the project has achieved some moderate success, with 210,000 visitors a month, and 45% of WHYY's total online revenue of $100,000 in fiscal 2011. The numbers fall far short of Philadelphia's online leader (Philly.com), which regularly attracts 7 million unique visitors a month. Similarly, the site's $45K in revenue pales in comparison with its reported $1.5 million operating budget.

NetNewsCheck has posted excerpts from an interview with WHYY's president and CEO, William Marrazzo, discussing the site's development, goals, and future. He provided three primary goals: to get some experience with hyperlocal portals; help in training multimedia newsmaking skills for their journalists; and to try to capture a younger audience to help grow their broadcast audiences. It's interesting that for a public service broadcaster, actually serving the public didn't seem to make the cut.

Source: "Could WHYY Redefine Public Media's Role?", NetNews Check

NetNewsCheck has posted excerpts from an interview with WHYY's president and CEO, William Marrazzo, discussing the site's development, goals, and future. He provided three primary goals: to get some experience with hyperlocal portals; help in training multimedia newsmaking skills for their journalists; and to try to capture a younger audience to help grow their broadcast audiences. It's interesting that for a public service broadcaster, actually serving the public didn't seem to make the cut.

Source: "Could WHYY Redefine Public Media's Role?", NetNews Check

Goin' Mobile

This may be the year that mobile media takes off. Earlier this year, analysts predicted that more smartphones and tablets would be sold than desktops and laptops this year. A recent study of top media publications in the U.S. showed 84% delivered content optimized for mobiles (see earlier post), and a post yesterday talked about how one news junkie now primarily uses mobile media to keep informed.

Now comes research on how people use mobile and other media, conducted by Flurry Analytics. As of this month, people spend an average of 81 minutes a day with mobile apps, compared with 74 minutes on the Web.

The new numbers on apps reflects a 91% increase in time spent on apps since last June. Analysts at Flurry used Internet usage data from comScore and Alexa, and their own app usage data. The data suggested that most of the increased app usage came as a result of more frequent sessions rather than a surge in session length. Time spent on the Internet also increased, but at a much slower rate (16%).

The data on app usage found that games and social media apps accounted for almost 80% of time spent. Facebook alone accounts for almost one-fifth of all time spent using mobile apps. Users also tended to go to game and social media apps more frequently, and spent more time per session, than other types of apps. News apps accounted for 9%, a distant third. A comScore report showed that 38% of all U.S. mobile users had downloaded and used apps, with more than a quarter accessing social media, and a quarter playing games. Still, in total numbers, the Internet's online audience of 216 million eclipses the roughly 75 million smartphone users.

The data on app usage found that games and social media apps accounted for almost 80% of time spent. Facebook alone accounts for almost one-fifth of all time spent using mobile apps. Users also tended to go to game and social media apps more frequently, and spent more time per session, than other types of apps. News apps accounted for 9%, a distant third. A comScore report showed that 38% of all U.S. mobile users had downloaded and used apps, with more than a quarter accessing social media, and a quarter playing games. Still, in total numbers, the Internet's online audience of 216 million eclipses the roughly 75 million smartphone users.

With the continuing boom in mobile platforms (smartphones and tablets), and the continuing diffusion of broadband networks for access, look for mobile media opportunities to also continue to grow significantly over the near future. The rise and growth in app usage offers new opportunities, and revenue potential, for existing media to exploit.

Source: "Time Spent on Apps Outpaces Web," Online Media Daily

"Mobile Apps Put the Web in Their Rear-view Mirror", Flurry.com blog

Now comes research on how people use mobile and other media, conducted by Flurry Analytics. As of this month, people spend an average of 81 minutes a day with mobile apps, compared with 74 minutes on the Web.

The new numbers on apps reflects a 91% increase in time spent on apps since last June. Analysts at Flurry used Internet usage data from comScore and Alexa, and their own app usage data. The data suggested that most of the increased app usage came as a result of more frequent sessions rather than a surge in session length. Time spent on the Internet also increased, but at a much slower rate (16%).

With the continuing boom in mobile platforms (smartphones and tablets), and the continuing diffusion of broadband networks for access, look for mobile media opportunities to also continue to grow significantly over the near future. The rise and growth in app usage offers new opportunities, and revenue potential, for existing media to exploit.

Source: "Time Spent on Apps Outpaces Web," Online Media Daily

"Mobile Apps Put the Web in Their Rear-view Mirror", Flurry.com blog

Monday, June 20, 2011

Video Viewing at Record Levels

In May, according to a Nielsen report, 15 billion videos were viewed online, surpassing April's record of 14 billion. Online video reach in the U.S. tops 145 million, and number of streams per month up 2% that month. There also seemed to be a small trend towards longer-form videos. For me, the surprise was the two newer services (uStream and Justin.tv) which allows users to share their own streamed content with the world.

Source: "Video Viewing At Record Highs", VidBlog

Source: "Video Viewing At Record Highs", VidBlog

Ready for (dot)news?

The body overseeing Internet Domain names just voted to open up the domain naming system to new top-level domain names to new terms "in any language or script." Those names were originally limited to a few terms (.com, .net, .org, .edu, .gov), and have added a few at a time to the current 22 options, plus about 250 country-level domains. While not a free-for-all (you still have to apply to ICANN to have the new domain label approved), it should make things interesting for a while. For example, who will be allowed to register domain names within the newly approved top-level domain names? I can imagine the fight over .apple, or the issue of whether the holder of registrations for a new '.news' top-level domain will get to decide which organizations qualify as "news" sites.

Opening up the system might have implications for continuing to promote global access. The "any language or script" is partially an outgrowth of efforts to move ICANN and the Internet from US/English language dominance. It could easily benefit users of those languages and scripts, assuming the availability of appropriate keyboards. On the other hand, having site addresses in other languages or scripts may make accessing sites more difficult for 'outsiders', or at least will tend to push having multiple site names in multiple languages and scripts, and greater reliance on Web and point-and-click interfaces.

Source: "Global Internet body to unleash domain names," Broadcast Newsroom.

Opening up the system might have implications for continuing to promote global access. The "any language or script" is partially an outgrowth of efforts to move ICANN and the Internet from US/English language dominance. It could easily benefit users of those languages and scripts, assuming the availability of appropriate keyboards. On the other hand, having site addresses in other languages or scripts may make accessing sites more difficult for 'outsiders', or at least will tend to push having multiple site names in multiple languages and scripts, and greater reliance on Web and point-and-click interfaces.

Source: "Global Internet body to unleash domain names," Broadcast Newsroom.

The New News Junkie

How can a news junkie remain informed without subscribing to any newspaper and not watching news on TV? These days, it's easier than you might think - if you're connected. In a piece for MacWorld, Lex Friedman writes on how he uses the Internet to keep informed, doing most of his reading through his iPad.

The article is worth a read, but the main point is Friedman takes advantage of RSS subscriptions to have headlines and stories sent from news sites as they're posted, and several apps to improve readability and archiving. Twitter gives an increasingly good window on breaking news and stories. These let him keep track of key focus areas. But Friedman also recognizes that news aggregators, like newspapers and TV news, by gathering broadly (rather than more narrow RSS focus) can expose you to other interesting items. And as they say, "There's apps for that." Friedman notes he does have several old media news apps (NY Times, Reuters, CNN, USA Today) in a folder; they aren't daily reads for him - more a set of places to go for different takes on stories. The story mentions a number of apps, as do some of the comments.

The Internet can certainly bring news faster than most any other medium, and can offer access to more detail and depth on stories than most media can afford to bring. On the other hand, there's still value in news judgment and the vetting of information that used to be the emphasis of journalism. It would seem to be a good mix, but Friedman notes that most old media news sites aren't very user-friendly - hard to navigate, too full of content to sift through, and rarely helpful in pointing to other sources of information. Almost as if their mindset is still in the analog mass media world, rather than embracing the potential for user-customization online news could provide.

Source: "How a news junkie uses the iPad," MacWorld

The article is worth a read, but the main point is Friedman takes advantage of RSS subscriptions to have headlines and stories sent from news sites as they're posted, and several apps to improve readability and archiving. Twitter gives an increasingly good window on breaking news and stories. These let him keep track of key focus areas. But Friedman also recognizes that news aggregators, like newspapers and TV news, by gathering broadly (rather than more narrow RSS focus) can expose you to other interesting items. And as they say, "There's apps for that." Friedman notes he does have several old media news apps (NY Times, Reuters, CNN, USA Today) in a folder; they aren't daily reads for him - more a set of places to go for different takes on stories. The story mentions a number of apps, as do some of the comments.

The Internet can certainly bring news faster than most any other medium, and can offer access to more detail and depth on stories than most media can afford to bring. On the other hand, there's still value in news judgment and the vetting of information that used to be the emphasis of journalism. It would seem to be a good mix, but Friedman notes that most old media news sites aren't very user-friendly - hard to navigate, too full of content to sift through, and rarely helpful in pointing to other sources of information. Almost as if their mindset is still in the analog mass media world, rather than embracing the potential for user-customization online news could provide.

Source: "How a news junkie uses the iPad," MacWorld

Cable Wins! (Fun with Numbers)

Cable networks proudly announced that cable networks grabbed more upfront advertising dollars (commitments from advertisers for the upcoming season) than the broadcast networks were able to generate. Cable got $8.96 billion compared to broadcast's $8.5 billion, with 20% of cable's upfront inventory still unsold.

On the other hand, the broadcast network number was only for prime time while the roughly 70 ad-supported networks were counting all day-parts. Then again, broadcast networks seem to be dropping out of a lot of mid-day and overnight day-parts, so it's a not unreasonable schedule vs. schedule comparison.

Source: "Cable's Big Headlines This Upfront: Continued Good News, Or A More Complex Story?" TVWatch

On the other hand, the broadcast network number was only for prime time while the roughly 70 ad-supported networks were counting all day-parts. Then again, broadcast networks seem to be dropping out of a lot of mid-day and overnight day-parts, so it's a not unreasonable schedule vs. schedule comparison.

Source: "Cable's Big Headlines This Upfront: Continued Good News, Or A More Complex Story?" TVWatch

Digital Audience Measurement Principles Proposed

I've had a few posts recently ( here, here, and here ) dealing with audience measurement issues, particularly those arising from a competitive, converged, and convoluted media environment. The issues are well known, and you can point to a number of attempts to address them. Last week, three key ad industry associations (4As, Ass. of National Advertisers, and the Interactive Ad Bureau) released a set of Guiding Principles they hope that those developing measures take to heart.

Source: "ANA, 4As, IAB Release Digital Measurement Principles." Online Media Daily

- Count real "viewable impressions" online. (some online measures count ads sent, and with screening software, they may or may not actually be seen)

- Count audiences, not eyeballs. (as advertisers increasingly target, measurement should be able to measure target audiences, not just screens)

- Create transparent classification systems (online ads come in myriad forms and sizes - need a system that allows comparisons)

- Develop "metrics that matter" for interactivity. (Brand marketers want measure of involvement, not viewing).

- Digital media measurements should be comparable to, and integrated with, other media. (would improve comparability with other media, and facilitate cross-media marketing)

Source: "ANA, 4As, IAB Release Digital Measurement Principles." Online Media Daily

Thursday, June 16, 2011

Taking Content Mobile

A study of the top 100 media publications in the U.S. shows 84% reaching out to mobile readers through some combination of mobile apps or websites optimized for mobile. Newspapers are leading the way, with 86% having a mobile site, and 92% having one or more smartphone apps. Consumer magazines were the least likely to have mobile websites (44%), but 62% had at least one type of smartphone app. Bloggers were more likely to have mobile versions of their websites (64%), with less than 40% having dedicated mobile apps.

On the smartphone side, iPhone apps dominated, with twice as many media having iPhone apps than Android apps (Blackberry was a close third among newspapers, but a distant third for consumer magazines and blogs.) Interestingly, media have been somewhat slow to monetize mobile services - most blog and consumer magazine mobile websites carry no advertising, nor do a quarter of newspaper sites.

The study also looked at mobile content, finding a focus on providing current and breaking news, leaving traditional items such as features and editorials to print and online properties.

As an interesting side note, the study showed that while U.S. media outlets have been quick to embrace mobile opportunities, only 11% of some 719 UK print media titles had mobile websites.

Sources: "Mobile Media Marketing", Research Brief from the Center for Media Research

Press release on study

On the smartphone side, iPhone apps dominated, with twice as many media having iPhone apps than Android apps (Blackberry was a close third among newspapers, but a distant third for consumer magazines and blogs.) Interestingly, media have been somewhat slow to monetize mobile services - most blog and consumer magazine mobile websites carry no advertising, nor do a quarter of newspaper sites.

The study also looked at mobile content, finding a focus on providing current and breaking news, leaving traditional items such as features and editorials to print and online properties.

As an interesting side note, the study showed that while U.S. media outlets have been quick to embrace mobile opportunities, only 11% of some 719 UK print media titles had mobile websites.

Sources: "Mobile Media Marketing", Research Brief from the Center for Media Research

Press release on study

Wednesday, June 15, 2011

IPTV Challenges Cable

More news on the emerging transition in TV from traditional broadcasting and multichannel services to IPTV..

Netflix is emerging as a driving force pushing IPTV. A new study shows that Netflix users are twice as likely (this year as compared to last) to degrade or cancel cable subscriptions. Meanwhile, content licensing is becoming more competitive, with Netflix making exclusive deals for TV programming. While cable creates walled gardens limiting access to other services, and touts "TV everywhere" at some point in the future, Netflix is already there, with its service offered on more than 250 devices, some of which offer a dedicated Netflix button on the remote..

Meanwhile, a new report from Nielsen concludes that there's a new trend in homes with both TV and Interent access shows that

To pile on the bad news for traditional TV, a new Harris Interactive Poll for Adweek looked at media and online video use and attitudes towards the Internet's relationship to TV. The results showed broad increases in online video use, with 77% indicating they've watched shows online. Use was highest in the 18-34 demographic (at 88%), but remained high for all demographic segments, all the way through the 55+ segment (64% have watched). In addition, about half indicated that they have watched shows online that they had not previously seen on TV, suggesting expanding choice options online. Wide adoption of online video makes IPTV a stronger competitor to cable and DBS services. In fact, 44% of respondents said they would cancel cable if they could get the shows they liked online for free. That number falls to 16% if their shows were only available online for a small fee. Still, at a time when cable has been losing subscribers consistently for years, and IP-delivered video choices are increasing (with AT&T's U-verse and the rise of streaming providers), of it's not good news for cable and DBS.

If this wasn't bad enough, consider the continued maturation of user-generated-content (UGC) and UGC-sharing sites like YouTube. Improvements in technology enable users to create higher-quality content. In addition, YouTube and similar sites are providing opportunities for the distribution of professional quality content and traditional TV programming. The programming options and reach of UGC channels are only getting bigger, and a lot of content is getting better, making it a stronger competitor to traditional TV for both audiences and advertisers.

All these show an improvement in the access to IPTV, and improvements in its value coming from better content, more programming options, and more choice in when and where viewing occurs. While cable and DBS can respond to some of these, an emphasize on keeping subscribers tied to their services is not helpful. Look for a continued decline in cable and other multichannel services, and continued expansion of IPTV as a delivery system for video.

Sources:

"Who are we kidding? Of course it's Netflix vs. cable," Gigacom

"Heavy Streaming Vidoe Viewers Watch Less TV, Nielsen Says" Media Daily News.

"Turner Discloses Tens of Thousands Of Online Viewers Being Added To Its TV Ratings" Media Daily News

"Survey: Sure, We'll Ditch Cable... Make an Offer!" Vidblog

"UGC Is All Grown Up!" Online Spin

Netflix is emerging as a driving force pushing IPTV. A new study shows that Netflix users are twice as likely (this year as compared to last) to degrade or cancel cable subscriptions. Meanwhile, content licensing is becoming more competitive, with Netflix making exclusive deals for TV programming. While cable creates walled gardens limiting access to other services, and touts "TV everywhere" at some point in the future, Netflix is already there, with its service offered on more than 250 devices, some of which offer a dedicated Netflix button on the remote..

Meanwhile, a new report from Nielsen concludes that there's a new trend in homes with both TV and Interent access shows that

the lightest traditional television users streaming significantly more Internet video via their computers, and the heaviest streamers under-indexing for traditional TV viewership. This behavior is led by those ages 18-34... while certain segments of the population are migrating toward specific services and viewing habits, the resounding trend is (for slight increases in total viewing across screens)Nielsen's new C3 ratings are also showing significant numbers of additional viewers coming from online viewing. A CNN executive reported that more than 50 individual telecasts saw significant ratings improvements with the addition of online viewers.

To pile on the bad news for traditional TV, a new Harris Interactive Poll for Adweek looked at media and online video use and attitudes towards the Internet's relationship to TV. The results showed broad increases in online video use, with 77% indicating they've watched shows online. Use was highest in the 18-34 demographic (at 88%), but remained high for all demographic segments, all the way through the 55+ segment (64% have watched). In addition, about half indicated that they have watched shows online that they had not previously seen on TV, suggesting expanding choice options online. Wide adoption of online video makes IPTV a stronger competitor to cable and DBS services. In fact, 44% of respondents said they would cancel cable if they could get the shows they liked online for free. That number falls to 16% if their shows were only available online for a small fee. Still, at a time when cable has been losing subscribers consistently for years, and IP-delivered video choices are increasing (with AT&T's U-verse and the rise of streaming providers), of it's not good news for cable and DBS.

If this wasn't bad enough, consider the continued maturation of user-generated-content (UGC) and UGC-sharing sites like YouTube. Improvements in technology enable users to create higher-quality content. In addition, YouTube and similar sites are providing opportunities for the distribution of professional quality content and traditional TV programming. The programming options and reach of UGC channels are only getting bigger, and a lot of content is getting better, making it a stronger competitor to traditional TV for both audiences and advertisers.

All these show an improvement in the access to IPTV, and improvements in its value coming from better content, more programming options, and more choice in when and where viewing occurs. While cable and DBS can respond to some of these, an emphasize on keeping subscribers tied to their services is not helpful. Look for a continued decline in cable and other multichannel services, and continued expansion of IPTV as a delivery system for video.

Sources:

"Who are we kidding? Of course it's Netflix vs. cable," Gigacom

"Heavy Streaming Vidoe Viewers Watch Less TV, Nielsen Says" Media Daily News.

"Turner Discloses Tens of Thousands Of Online Viewers Being Added To Its TV Ratings" Media Daily News

"Survey: Sure, We'll Ditch Cable... Make an Offer!" Vidblog

"UGC Is All Grown Up!" Online Spin

From Backpack to Pocket Journalism

Several of the larger US networks (CBS, CNN) have apps enabling individuals to record and submit multimedia content to intermediaries who might use some of it, but haven't widely used apps for direct filing of stories or live reports.

Sources: "BBC Developing iPhone App for Live Broadcasting", Mashable

"BBC Developing new iPhone app for field reporters," Journalism.co.uk

Tips for Content Creators

There's been a number of good posts and articles recently with ideas for getting the most from content. To keep the post short, I'll summarize the main points and encourage you to follow the links for more.

Barry Lowenthal addresses an emerging shift in audience behavior, where access is replacing ownership as a driving motivation in audience demand for media content. One implication for content creators - make sure your content is available both for sale and rent.

Nathan Lump looks at things you can do to make online video content easy to find and more accessible, by taking advantage of digital networks' search, recommendation, and sharing capabilities and the potential for building partnerships.

Darcey Topham builds on the enthusiasm for online video to remind folks that making content available to all screens means making sure that the content is optimized for the wide range of screen sizes, formats, resolutions, and software.

Arnel Leyva considers how content creators and distributors can use digital media optimization to increase the value of their products to advertisers,

Maria Popova looks at Twitter as a form of information curation and authorship - "as a medium of conversational direction and a discovery platform for the (content) and conversations that matter." For content creators, Twitter can be another means of promotion, a source for ideas, and a help in identifying trends..

The general thrust here is that in a competitive media environment, you want to try to make your content as valuable, as widely available, and as easily discoverable as possible. Getting it on the digital media network is a step, but there are things you can do to improve your odds of success.

Sources:

"I No Longer Want To Own Music. I Want To Be A Renter", Online Media Daily

"7 Ways to Get Your Content to Its Audience", Online Media Daily

"Online Video Content: Adapt for 'Any Screen' Consumption, or Bust". Online Video Insider

"Digital Media Optimization - The Advertising Afterthought", Online Media Daily

"In a new world of informational abundance, content curation is a new kind of authorship", Nieman Journalism Lab

Barry Lowenthal addresses an emerging shift in audience behavior, where access is replacing ownership as a driving motivation in audience demand for media content. One implication for content creators - make sure your content is available both for sale and rent.

Nathan Lump looks at things you can do to make online video content easy to find and more accessible, by taking advantage of digital networks' search, recommendation, and sharing capabilities and the potential for building partnerships.

Darcey Topham builds on the enthusiasm for online video to remind folks that making content available to all screens means making sure that the content is optimized for the wide range of screen sizes, formats, resolutions, and software.

Arnel Leyva considers how content creators and distributors can use digital media optimization to increase the value of their products to advertisers,

Maria Popova looks at Twitter as a form of information curation and authorship - "as a medium of conversational direction and a discovery platform for the (content) and conversations that matter." For content creators, Twitter can be another means of promotion, a source for ideas, and a help in identifying trends..

The general thrust here is that in a competitive media environment, you want to try to make your content as valuable, as widely available, and as easily discoverable as possible. Getting it on the digital media network is a step, but there are things you can do to improve your odds of success.

Sources:

"I No Longer Want To Own Music. I Want To Be A Renter", Online Media Daily

"7 Ways to Get Your Content to Its Audience", Online Media Daily

"Online Video Content: Adapt for 'Any Screen' Consumption, or Bust". Online Video Insider

"Digital Media Optimization - The Advertising Afterthought", Online Media Daily

"In a new world of informational abundance, content curation is a new kind of authorship", Nieman Journalism Lab

Tuesday, June 14, 2011

More Privacy News

The Digital Advertising Alliance has added two of the larger groups representing ad agencies to a group working on the creation of privacy standards for Online Behavioral Advertising. The centerpiece and public face of the effort is the "Advertising Option" icon, which will be included in or with online ads, indicating participation in the program (and hopefully, adherence to the industry's self-imposed standards about privacy in the collection and use of online behavioral data).

Participation in the privacy standards program creates certain responsibilities on the part of various parts of the online advertising industry. For media and creative agencies, it means identifying what parts of the campaign incorporates online behavioral advertising, and ensuring a place to insert the icon and/or links to systems allowing users to opt-out. For ad networks and advertisers, it means an agreement to abide by the standards, providing an opt-out option and complying with user opt-out requests.

Participation in the privacy standards program creates certain responsibilities on the part of various parts of the online advertising industry. For media and creative agencies, it means identifying what parts of the campaign incorporates online behavioral advertising, and ensuring a place to insert the icon and/or links to systems allowing users to opt-out. For ad networks and advertisers, it means an agreement to abide by the standards, providing an opt-out option and complying with user opt-out requests.

It's a good sign that the industry has recognized and is addressing the issue of privacy, as the Internet offers abundant opportunity to amass data on its users.

I wish the program success.

Source: "Digital Ad Alliance Creates Privacy Rules for Online Ads", Online Media Daily

Website for the "Self-Regulatory Program for Online Behavioral Advertising."

(revised to remove typo and add Source link)

It's a good sign that the industry has recognized and is addressing the issue of privacy, as the Internet offers abundant opportunity to amass data on its users.

I wish the program success.

Source: "Digital Ad Alliance Creates Privacy Rules for Online Ads", Online Media Daily

Website for the "Self-Regulatory Program for Online Behavioral Advertising."

(revised to remove typo and add Source link)

Facebook - Trouble with Faces?

Some of the oldest and largest public interest/advocacy groups concerned about online privacy have asked the Federal Trade Commission to force Facebook to suspend operation of a new feature that uses facial recognition software to identify people appearing in other people's photos. The complaint argues that the automatic tagging system amounts to an automated online identification system that largely occurs outside of individual's knowledge or consent; and as such exposes individuals to unknown risks. The complaint calls for Facebook to obtain "opt-in" consent before sharing information about them in new ways.

Facebook has replied that it's previously announced its automatic tagging feature as it's become available in countries. They say that users can "opt-out" - that if you become concerned about particular applications of automatic tagging, you can reconfigure your privacy settings to not automatically tag your image (if you can figure out how). They also claim that if other users 'tag" you in their photos, you can ask for your name to be removed after the fact. [Opt-in permissions require specific consent be obtained prior to the collection and/or use of information, while opt-out permissions only stop the use or sharing of the information collected after notification that you've opted out]. Those backing the complaint argue that Facebook still hasn't provided adequate information about the range and extent of personal information that it collects on its users, and that the opt-out option fails to prevent continued collection of the biometric data, or require the deletion of data already collected. They say that Facebook has left open the potential for the service to market or share the data with advertisers, app developers, and the government without users' permission. Name searches could reveal information about you that you had no idea was there.

So the fundamental lesson about the Internet needs to be expanded. No longer do you need to realize that once you post things on the Internet, it's always out there somewhere, so be careful as to what you post. Now, you may also want to be careful about what your friends post - those potentially embarrassing photos your friends posted from last Spring Break may show up at a later job interview.

Source: "Privacy Groups File FTC Complaint About Face Recognition", Online Media Daily

Facebook has replied that it's previously announced its automatic tagging feature as it's become available in countries. They say that users can "opt-out" - that if you become concerned about particular applications of automatic tagging, you can reconfigure your privacy settings to not automatically tag your image (if you can figure out how). They also claim that if other users 'tag" you in their photos, you can ask for your name to be removed after the fact. [Opt-in permissions require specific consent be obtained prior to the collection and/or use of information, while opt-out permissions only stop the use or sharing of the information collected after notification that you've opted out]. Those backing the complaint argue that Facebook still hasn't provided adequate information about the range and extent of personal information that it collects on its users, and that the opt-out option fails to prevent continued collection of the biometric data, or require the deletion of data already collected. They say that Facebook has left open the potential for the service to market or share the data with advertisers, app developers, and the government without users' permission. Name searches could reveal information about you that you had no idea was there.

So the fundamental lesson about the Internet needs to be expanded. No longer do you need to realize that once you post things on the Internet, it's always out there somewhere, so be careful as to what you post. Now, you may also want to be careful about what your friends post - those potentially embarrassing photos your friends posted from last Spring Break may show up at a later job interview.

Source: "Privacy Groups File FTC Complaint About Face Recognition", Online Media Daily

Net use in China

comScore recently released a report looking at how Internet users in Greater China (Mainland, Hong Kong, and Taiwan) spend their time online. Portals accounted for 24.4%, and another 6.2% was spent on search or navigation. Social networking accounted for 5.5% (a third of the global average), and retail sites accounted for another 5%.

Local or localized services were the primary sites within each category. Tencent, Inc. was the largest portal, reaching almost two-thirds of Internet users in Greater China. Baidu.com was the leading search site, totaling almost 60% of unique visitors. On the retail side, Alibaba.com led the way, being used by 36.5% of respondents. The Entertainment and Social Media categories seemed more competitive, with Youku the largest online video provider (used by 20%), and the Oak Pacific Interactive sites (including Renren.com) used by 18%. On the other hand, those numbers are for all Internet users, not proportions of use within categories.

Overall, Internet use is expanding rapidly in China, and the PRC recently became the country with the largest number of Internet users. Still, Internet access remains largely limited to urban areas, with most users accessing through Internet cafes or mobile devices. Most large US Internet services have tried the China market, although they have found that government restrictions, language conflicts, and strong local competition have limited their success.

Source: "Portals and Entertainment Top Web Categories in China", Research Brief (a MediaPost Blog)

Local or localized services were the primary sites within each category. Tencent, Inc. was the largest portal, reaching almost two-thirds of Internet users in Greater China. Baidu.com was the leading search site, totaling almost 60% of unique visitors. On the retail side, Alibaba.com led the way, being used by 36.5% of respondents. The Entertainment and Social Media categories seemed more competitive, with Youku the largest online video provider (used by 20%), and the Oak Pacific Interactive sites (including Renren.com) used by 18%. On the other hand, those numbers are for all Internet users, not proportions of use within categories.

Overall, Internet use is expanding rapidly in China, and the PRC recently became the country with the largest number of Internet users. Still, Internet access remains largely limited to urban areas, with most users accessing through Internet cafes or mobile devices. Most large US Internet services have tried the China market, although they have found that government restrictions, language conflicts, and strong local competition have limited their success.

Source: "Portals and Entertainment Top Web Categories in China", Research Brief (a MediaPost Blog)

"TV Everywhere" and Advertising

"Within two years, 75% of TV Content will be on other platforms." While that may seem to be a wild conjecture, representatives from Disney/ESPN, Comcast, and Turner Broadcasting made that statement at the Elevate Video Advertising Summit last week. "TV Everywhere" seemed imminent, and specific distribution outlet irrelevant - at least if two issues get resolved (licensing rights, and advertising measurement). The second issue was the focus at the conference.

There are two problems arising from the expansion of distribution and the shift in audience viewing habits. The first is that, for now, online video advertising levels and rates are significantly lower than in traditional media. There is concern that as viewing shifts, total ad revenue will fall. Second, and more fundamental, is that most measurement systems (ratings) actually measure exposure to the programming that ads are embedded in. If program exposure begins to be split among a variety of options (multiple showings on multiple networks, online viewing, delayed viewing, etc.), how can all that be measured? More importantly from the advertiser's perspective is this issue - unless the ad is embedded in the programming, or otherwise present in all the myriad viewing options, then measures of program exposure (ratings) are no longer a viable substitute for exposure to advertising. Ratings then become less useful and valuable for advertisers, and ad buying based on those measures become riskier (which would drive prices down).

Will online ad rates and revenues quickly match those of traditional broadcasters? The consensus at the conference was, not soon, if ever - there are good economic reasons for differential rates.. But total revenues are likely to converge over time (some projections show total online ad revenues passing TV ad revenues by 2021). Right now, TV gets $70 billion in ad dollars, while online video generates $1.5 billion. Some of that reflects levels of viewing (audience). But advertising isn't just one generic market - it's well-known that advertisers will pay a premium for appropriately targeted audiences. What is discussed less, is that there is a separate (and sizable) ad market for large general audiences - just like some advertisers want targets, others want a more broad-based reach. They may not value that more (on a per person basis), but it is a separate added demand fighting for a fixed advertising supply on a relative few TV channels that can deliver that level of exposure. The big general-interest channels have an additional layer of demand, and the increased demand drives up the prices they can get, and thus higher revenues. This is illustrated by the ad market for the SuperBowl. Online video's strength is in targeting, not in reaching the large, general-interest audience. Even now, online video ad revenues are prioritized more or less this way: Broadcasters; Internet portals (Yahoo, Google, YouTube), followed by ad networks and video publishers..

Finding good content and advertising exposure measures has been difficult to do (I addressed that issue earlier, here, here, and here). One fundamental problem is that as competition shrinks audience, media firms have looked to inflate the numbers by including other content distribution and use. But, unless the same ads are included with all of the added distribution forms and uses, those measures become less and less useful for advertisers. Another concern has been accuracy, both in terms of overall numbers, and in the ability to deliver targeted advertising as promised. A new report from Nielsen's Online Campaign Ratings service found than targeted campaigns based on an age range of less than 20 years delivered that audience only 30% of the time (for larger age ranges, it was still only 77%). Targeting by gender and age reached the intended audience slightly more than a quarter of the time. Both media and industry has been working on coming up with new, hopefully more appropriate, measures, but getting consensus and acceptance has been difficult.

Sources: "As Video Distribution Becomes Ubiquitous, Advertising Differences Become Blurry," Online Video Insider

"Online Campaigns Miss Targets, Need Better Measurements," Online Media Daily

There are two problems arising from the expansion of distribution and the shift in audience viewing habits. The first is that, for now, online video advertising levels and rates are significantly lower than in traditional media. There is concern that as viewing shifts, total ad revenue will fall. Second, and more fundamental, is that most measurement systems (ratings) actually measure exposure to the programming that ads are embedded in. If program exposure begins to be split among a variety of options (multiple showings on multiple networks, online viewing, delayed viewing, etc.), how can all that be measured? More importantly from the advertiser's perspective is this issue - unless the ad is embedded in the programming, or otherwise present in all the myriad viewing options, then measures of program exposure (ratings) are no longer a viable substitute for exposure to advertising. Ratings then become less useful and valuable for advertisers, and ad buying based on those measures become riskier (which would drive prices down).

Will online ad rates and revenues quickly match those of traditional broadcasters? The consensus at the conference was, not soon, if ever - there are good economic reasons for differential rates.. But total revenues are likely to converge over time (some projections show total online ad revenues passing TV ad revenues by 2021). Right now, TV gets $70 billion in ad dollars, while online video generates $1.5 billion. Some of that reflects levels of viewing (audience). But advertising isn't just one generic market - it's well-known that advertisers will pay a premium for appropriately targeted audiences. What is discussed less, is that there is a separate (and sizable) ad market for large general audiences - just like some advertisers want targets, others want a more broad-based reach. They may not value that more (on a per person basis), but it is a separate added demand fighting for a fixed advertising supply on a relative few TV channels that can deliver that level of exposure. The big general-interest channels have an additional layer of demand, and the increased demand drives up the prices they can get, and thus higher revenues. This is illustrated by the ad market for the SuperBowl. Online video's strength is in targeting, not in reaching the large, general-interest audience. Even now, online video ad revenues are prioritized more or less this way: Broadcasters; Internet portals (Yahoo, Google, YouTube), followed by ad networks and video publishers..

Finding good content and advertising exposure measures has been difficult to do (I addressed that issue earlier, here, here, and here). One fundamental problem is that as competition shrinks audience, media firms have looked to inflate the numbers by including other content distribution and use. But, unless the same ads are included with all of the added distribution forms and uses, those measures become less and less useful for advertisers. Another concern has been accuracy, both in terms of overall numbers, and in the ability to deliver targeted advertising as promised. A new report from Nielsen's Online Campaign Ratings service found than targeted campaigns based on an age range of less than 20 years delivered that audience only 30% of the time (for larger age ranges, it was still only 77%). Targeting by gender and age reached the intended audience slightly more than a quarter of the time. Both media and industry has been working on coming up with new, hopefully more appropriate, measures, but getting consensus and acceptance has been difficult.

Sources: "As Video Distribution Becomes Ubiquitous, Advertising Differences Become Blurry," Online Video Insider